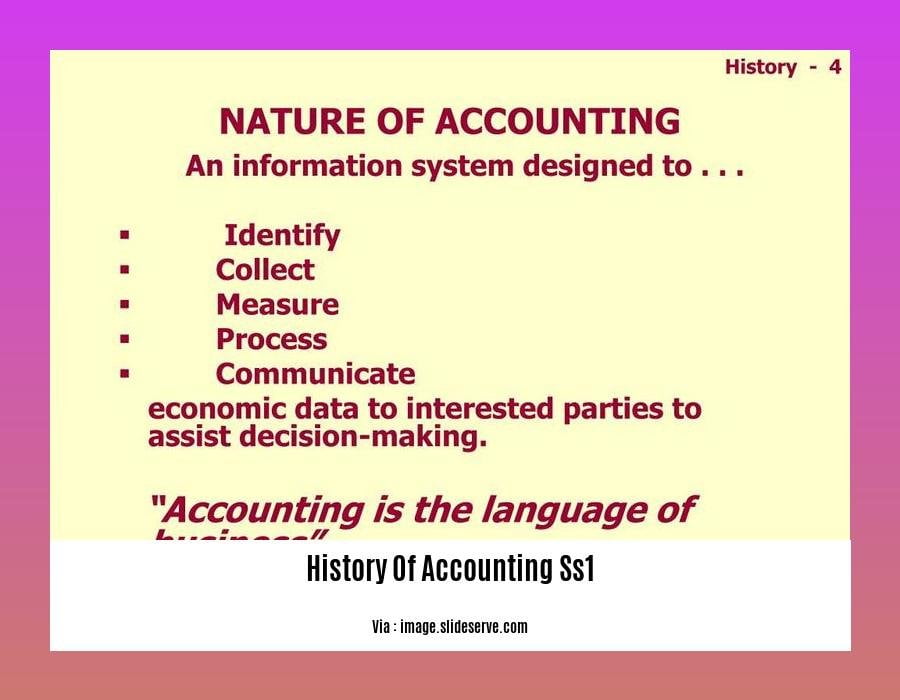

Embark on a captivating journey through the annals of financial history in [[History of Accounting SS1]: A Journey Through the Evolution of Financial Practices]. Delve into the fascinating evolution of accounting practices, tracing their profound impact on the business landscape from ancient civilizations to the digital age. Discover how accounting has shaped the way we manage, analyze, and report financial information, laying the foundation for the modern financial systems that underpin our global economy.

Key Takeaways:

Accounting has ancient roots; civilizations like Mesopotamia, Egypt, and Greece tracked transactions using basic accounting techniques on clay tablets.

Luca Pacioli, an Italian mathematician, revolutionized accounting by publishing the first work on double-entry bookkeeping.

Early accounting systems developed in Greece, Rome, and the Islamic world, with governments relying on detailed financial information for decision-making.

Over time, accounting practices evolved to meet the needs of businesses and organizations in various industries, reflecting changing economic and financial landscapes.

The history of accounting offers valuable insights into the evolution of financial practices and their impact on our understanding of business and economics today.

History of Accounting SS1: A Journey Through Financial Evolution

Have you ever pondered the roots of accounting, a practice that has shaped civilizations since ancient times? Join us on an enlightening journey as we delve into the rich history of accounting, exploring its humble origins and transformative impact on the business landscape.

The Dawn of Accounting:

In the bustling marketplaces of ancient Mesopotamia, scribes diligently etched transactions onto clay tablets, laying the foundation for accounting practices. These rudimentary records served as a means of tracking goods, ensuring fair trade, and preserving financial information for posterity.

Greek and Roman Contributions:

As civilizations flourished in Greece and Rome, accounting systems gained sophistication. The Greeks introduced the concept of accountability, while the Romans developed intricate record-keeping methods for their vast empire. These advancements laid the groundwork for the standardized accounting practices we rely on today.

The Renaissance Revolution:

A pivotal moment in accounting history occurred during the Italian Renaissance. Luca Pacioli, a renowned mathematician and Franciscan friar, published his groundbreaking treatise, Summa de Arithmetica, Geometria, Proportioni et Proportionalita. This seminal work introduced the concept of double-entry bookkeeping, revolutionizing the field of accounting.

The Industrial Revolution and Beyond:

The Industrial Revolution ushered in a new era of economic growth and complexity. The rise of corporations and joint-stock companies necessitated the development of more robust accounting systems to track assets, liabilities, and profits. Accountants became indispensable in ensuring the financial health and transparency of these growing enterprises.

The Digital Age:

In the modern era, technology has transformed accounting practices once again. The advent of computers, cloud-based software, and artificial intelligence has streamlined financial processes, automated tasks, and enhanced the efficiency and accuracy of accounting.

As we stand on the threshold of the 21st century, accounting continues to evolve, adapting to the ever-changing demands of the global economy. From the clay tablets of antiquity to the digital ledgers of today, the history of accounting is a testament to the enduring importance of accurate financial record-keeping.

For an amazing overview of the evolution and regulations of basketball, check out history and rules of basketball. They have a compilation of interesting historical anecdotes and a thorough explanation of the game’s rules. And if you are interested in knowing about the history and origin of the famous Adowa dance, visit here history of adowa dance, to discover the fascinating story behind this vibrant and expressive traditional dance.

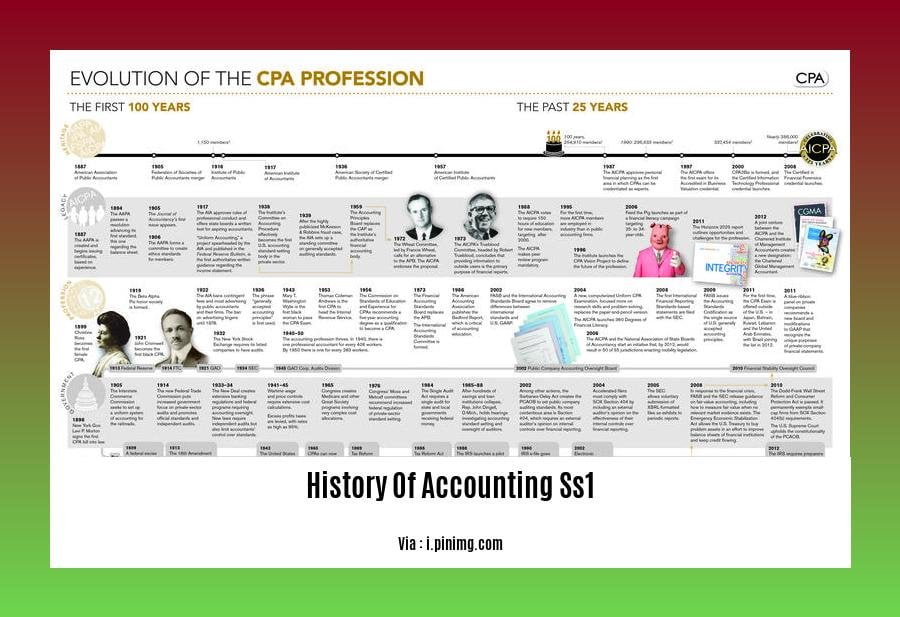

The Development of Accounting Standards and Regulations in the 19th and 20th Centuries

The world of accounting is a fascinating one, filled with a rich tapestry of history and evolution. Standards and regulations in the field have taken shape over centuries, influenced by innovations and market needs. In the 19th and 20th centuries, these influences were felt particularly strongly.

A Journey of Transformation: The 19th Century

A pivotal moment in accounting history occurred in the 19th century when the Industrial Revolution took hold. Industrialists realized that effective financial management was pivotal to their success, giving rise to the need for uniformity and transparency in financial reporting. This birthed the initial efforts to establish accounting standards and regulations.

The 20th Century: A Surge of Standardization

The 20th century witnessed a surge in the development of accounting standards and regulations. Here are some significant milestones that shaped the landscape:

1. The Committee on Accounting Procedure (CAP): Established in 1939, the CAP was a significant player in setting accounting standards in the United States.

2. The American Institute of Certified Public Accountants (AICPA): The AICPA played a crucial role in promoting ethical accounting practices and issuing accounting principles.

3. The Securities and Exchange Commission (SEC): The SEC’s formation in 1934 ushered in a new era of financial regulations, requiring publicly traded companies to submit financial statements prepared according to specific standards.

4. The Accounting Principles Board (APB): The APB, formed in 1959, continued the work of the CAP, issuing important standards such as APB Opinion No. 11, which established the principle of materiality.

5. The Financial Accounting Standards Board (FASB): In 1973, the FASB replaced the APB and became the primary body responsible for setting accounting standards in the United States.

6. International Accounting Standards Board (IASB): The creation of the IASB pushed for global harmonization of accounting standards, leading to the development of International Financial Reporting Standards (IFRS).

Key Takeaways:

The 19th century saw an increased need for accounting standards and regulations due to the Industrial Revolution.

The 20th century witnessed significant developments in accounting standards and regulations, including the formation of influential organizations like the CAP, AICPA, SEC, APB, and FASB.

The establishment of the FASB and the IASB marked a new era of financial reporting standardization, both domestically and internationally.

The evolution of accounting standards and regulations in the 19th and 20th centuries laid the foundation for the modern financial reporting landscape.

The influence of the Industrial Revolution and the rise of corporations on accounting practices

Before the Industrial Revolution, accounting was largely focused on tracking and managing personal finances, with little emphasis on complex business transactions. However, with the advent of industrialization, the need for accurate and efficient accounting practices became paramount.

The following are some key points to consider:

Increased Business Complexity:

The Industrial Revolution ushered in a surge of new business enterprises and industries, each with intricate financial dealings that required systematic recording and analysis.

Cost Accounting:

To ensure efficient production and profitability, businesses needed to accurately determine the costs associated with manufacturing their goods. Cost accounting emerged as a critical tool for managing and controlling these costs.

Standardization:

With the rise of joint-stock companies and the need to attract investors, there arose a demand for standardized accounting practices that would allow for transparent and comparable financial reporting.

Regulation:

To protect investors and ensure the reliability of financial information, various accounting organizations were established to regulate the profession and promote ethical standards.

Key Takeaways:

The Industrial Revolution fueled the need for robust accounting practices to manage complex business transactions.

Cost accounting became essential for determining production costs and ensuring profitability.

Standardization of accounting practices facilitated transparent financial reporting and attracted investors.

The establishment of accounting organizations promoted ethical practices and protected investor interests.

Sources:

The Impact of Industrial Revolution on Accounting – LinkedIn

The impact of technology on Accounting in the modern era

Technology has revolutionized the way accounting is done today. From automating tasks to enhancing efficiency, the impact of technology cannot be ignored. It has brought several significant changes to the field of accounting, including:

1. Automation of Accounting Tasks

Manual data entry and calculations were time-consuming. Computers have streamlined these processes, reducing the time spent on repetitive tasks. It has enabled accountants to focus more on analysis and interpretation of financial data.

2. Improved Efficiency

Computerized systems allow for faster processing of financial transactions. The integration of accounting software with other business applications has further improved efficiency by automating data transfer between different systems.

3. Increased Accuracy

Automated systems reduce errors caused by human mistakes. They ensure consistency and accuracy in financial calculations and reporting.

4. Enhanced Data Accessibility

Cloud-based accounting software allows accountants to access financial data from anywhere. This has facilitated collaboration and real-time decision making.

5. Improved Data Security

Technology has enabled the implementation of robust security measures to protect sensitive financial information.

6. Expansion of the Role of Accountants

Accountants now play a more strategic role in organizations. With technology handling routine tasks, they can dedicate more time to providing insights, making them indispensable in business decision-making.

7. Increased Accessibility for Small Businesses

Small businesses, which traditionally did not have the resources for robust accounting systems, now have access to affordable and user-friendly cloud-based accounting software.

8. Emergence of Data Analytics

Technology has brought forth powerful data analytics tools. Accountants can now analyze financial data, identify trends, and make predictions, enabling proactive decision-making.

Key Takeaways:

Technology has automated tasks, improved efficiency, and increased accuracy in accounting.

Cloud-based accounting software allows for data access, collaboration, and real-time decision making.

Technology has enabled accountants to shift from routine tasks to strategic roles, focusing on analysis and insights.

Small businesses now have access to affordable and user-friendly accounting software.

Data analytics tools enable accountants to identify trends and make predictions, enabling proactive decision-making.

Sources:

– The Impact of Technology on Accounting

How Technology Is Transforming the Role of Accountants

FAQ

Q1: How did ancient civilizations contribute to the history of accounting?

A1: Ancient civilizations, such as the Mesopotamians, Egyptians, and Greeks, used basic accounting techniques to track transactions on clay tablets. This laid the foundation for the development of more sophisticated accounting systems in later periods.

Q2: What was the significance of Luca Pacioli’s work in the history of accounting?

A2: Luca Pacioli, an Italian mathematician, published the first work on double-entry bookkeeping in 1494. This revolutionary concept transformed the field of accounting, providing a systematic and efficient way to record financial transactions and track assets and liabilities.

Q3: How did the Industrial Revolution impact the history of accounting?

A3: The Industrial Revolution brought about significant changes in the business landscape, leading to an increased need for accounting techniques and practices to manage complex business transactions. Accountants played a vital role in developing cost accounting systems, standardized accounting practices, and establishing professional accounting organizations.

Q4: What role did accountants play in the development of financial reporting standards?

A4: With the rise of joint-stock companies and the need for attracting investors, financial reporting requirements became more stringent. Accountants played a significant role in developing accounting standards and procedures to provide consistent and transparent financial information to investors and other stakeholders.

Q5: How has technology impacted the history of accounting?

A5: The impact of technology on accounting has been substantial, with computerized systems automating and streamlining many accounting tasks. Information technology has reduced the time required to prepare and present financial information, enabled the development of enterprise resource planning (ERP) systems, and transformed the way accountants connect with clients and access diverse roles.

Hello, My love for writing is rivaled only by my passion for in-depth research. While many may skim the surface, I dive deep, seeking the hidden gems of information that give a story texture and depth. Every word I write is backed by hours of exploration, ensuring that my work is not just compelling, but also meticulously accurate. Join me on a journey where every piece is a deep dive into the realms of knowledge and storytelling.